Hello again,

first of all, the comment by BeHaElJa ("so you are paying off €2000 and €1500 variable") referred to someone who had presented their financing plan in a previous post. That was NOT our plan.

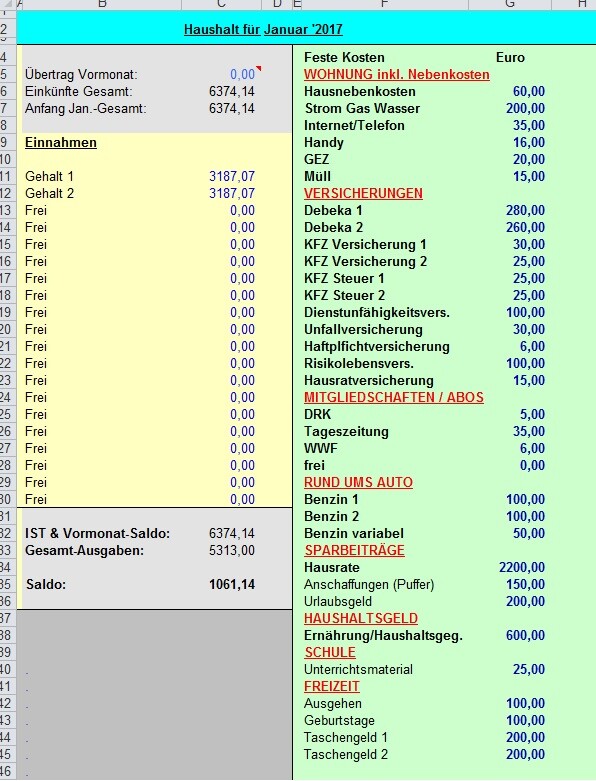

Attached I have included our household budget. Tax and insurance contributions, insofar as they are not paid monthly, have been broken down to the monthly amount.

Household Budget Variant 1 - married without children

The ancillary house costs include property tax and building insurance.

Electricity/gas/water relatively low – photovoltaic system on the roof, possibly air heat pump + battery storage, whether that works and makes sense still needs to be clarified. In any case, we want to achieve KFW 55 standard. Whether with gas or not, we will see then.

I have already slightly increased the private health insurance contributions as well as internet/phone, GEZ, garbage etc., in view of expected price increases.

For vehicle tax, I assumed two diesel vehicles in the Hamburg plan, which are currently also driven. However, for the coming years, two gasoline vehicles are planned.

The DU (which currently already exists) will be taken over by the employer in 2 years. However, we would like to insure ourselves additionally and will then be just under these €100.

The RLV contributions (declining variant) have already been calculated by our broker and will amount to €50 per month each with full loan coverage.

The other insurances are the same, the HRV was theoretically adjusted upwards.

The buffer for acquisitions is intended for washing or dishwashers, stove, faucet, car repairs, vehicle inspection or similar. For this, we would open a separate sub-account to which we would transfer everything left at the end of the month.

Vacation money is estimated at €200... with €2400 per year, we have managed quite well in recent years.

€600 Hamburg money includes expenses for food/drinks/personal and cleaning items. Currently, we are at €450 here and manage quite well with this. The better half would like to increase this item (organic products, meat from next door, etc.)

Pocket money would remain at €200 per person even after the house is built.

As a result, we would have around €1000 left with such a living standards, with which we could finance two cars (I calculate about €500 installment for both cars) and at the same time, considering the total two-year loss of income, put some aside (at least €10,000 have already been reserved for this).

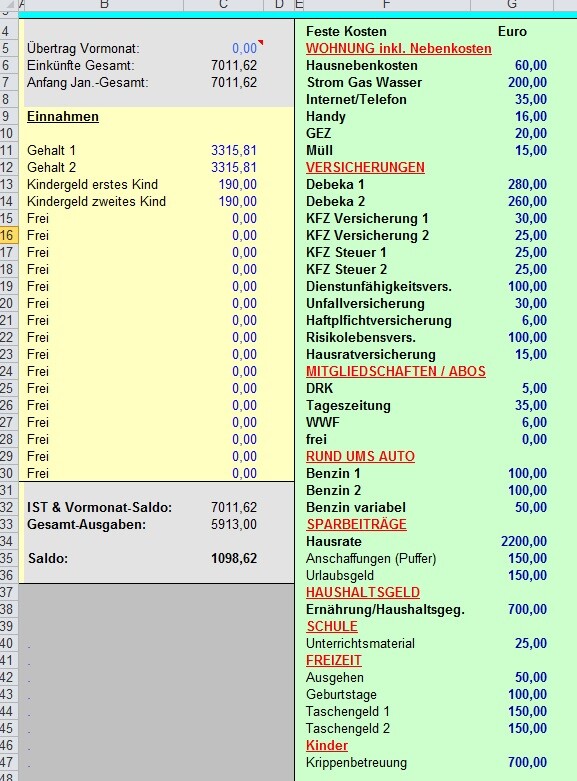

Variant 2 - married with 2 children

Basically, a similar picture here.

Income naturally increases, but on the other hand, there are additional costs for daycare and kindergarten care for a total of 5 years (the third year of kindergarten is free in this community).

The prospective grandparents (both just under 55 years old and employed) live 600m as the crow flies from both our potential house and the potential daycare or kindergarten place. We should find out as soon as possible how long we will have to wait for such a place.

Of course, income is lost in the year of home care. I just wanted to make it clear that after this dry spell (which we want to bridge as described), there would be enough money available again to make annual special repayments of about €10,000 as planned (we get about €5000 back in taxes per year).

Also important: Our balance when the daycare costs no longer apply. Then there is also enough money to fulfill the occasional wish of the children (who will at the latest get bigger in elementary school age).

Miscellaneous

The house would be completely ready for occupancy at €700,000. We would only need to put the furniture in, which we currently would not basically need to buy new from (of course then when children come).

According to the architect, at €700,000 we can assume a good middle-class standard... double glazing, plastic windows... still, "upgrade costs" are definitely a concern that we are still carrying with us..

I hope this information brings some more clarity and makes it easier to assess our project realistically.

As always, many thanks for reading and for your answers!