Numborner

2020-08-26 23:55:22

- #1

Hello,

we received an offer from an acquaintance at LBS and I would like to share it for comparison with the pure annuity loan and also have some comments.

I hope the many questions don’t annoy anyone, but with every piece of information we get, the uncertainty grows about what would be the "best" way to finance.

LBS option:

15 years fixed, then building savings contract

€250,000 interest loan/building savings contract at 0.99% = €828

€40,000 annuity loan at 1.04% = €240

total monthly rate = €1068

means the first 15 years = €1068 rate

the next 15 years = €1000 rate

Total costs

€43,000

€64,200

€250,000

----------

€357,200

- Advantage: after 15 years you have interest rate security with 2.2% until the end or if the interest rate is then cheaper, refinancing.

- you can possibly redeem the building savings contract if money is available

- flexible after 15 years

Annuity loan:

Annuity loan of €290,000

20 years fixed

1.25% effective interest rate

Rate €1065

5% special repayment possible

Remaining debt after 20 years = €80,000

Including interest, then €255,000 would have been paid after 20 years for €210,000 (290,000€-80,000€)

= €45,000 interest

We have now calculated how the financing of the remaining debt could look like, hope the calculations are correct

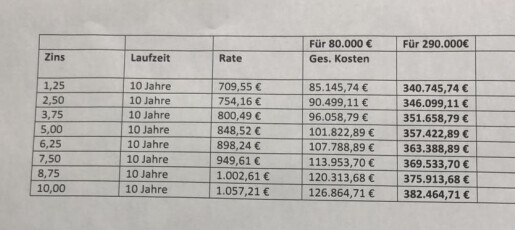

at 5% interest in 20 years a refinancing over 10 years would cost a total of €101,000, so a further €21,000 interest until the loan is paid off.

Total costs after the end of financing

1.25% refinancing = €340,000

3.75% refinancing = €351,000

5.00% refinancing = €357,000

etc.

Means, the interest rates would have to rise up to 4.5-5% in the 20 years for the total costs to be identical. Anything higher would make the annuity version more expensive.

I cannot directly see the "catch" of the building savings contract variant(s), but basically many are against building savings contracts.

Am I overlooking something or several factors?

Too many trees, you can’t see the forest anymore :)

If interest rates remain at 1.25% after 20 years, I would be cheaper compared to annuity loan + refinancing, if interest rates rise to 5% I am still identical to annuity loan + refinancing.

With building savings contract you could make higher special repayments, fully repay, etc. With annuity loan I am always bound for time x.

I am neither a fan nor opponent of building savings contracts, but annuity loans are preferred everywhere.

Have we made calculation errors in the whole matter or...

We are more than thankful for tips or advice, because soon we have to decide how to finance?

Greetings from Saarland

we received an offer from an acquaintance at LBS and I would like to share it for comparison with the pure annuity loan and also have some comments.

I hope the many questions don’t annoy anyone, but with every piece of information we get, the uncertainty grows about what would be the "best" way to finance.

LBS option:

15 years fixed, then building savings contract

€250,000 interest loan/building savings contract at 0.99% = €828

€40,000 annuity loan at 1.04% = €240

total monthly rate = €1068

means the first 15 years = €1068 rate

the next 15 years = €1000 rate

Total costs

€43,000

€64,200

€250,000

----------

€357,200

- Advantage: after 15 years you have interest rate security with 2.2% until the end or if the interest rate is then cheaper, refinancing.

- you can possibly redeem the building savings contract if money is available

- flexible after 15 years

Annuity loan:

Annuity loan of €290,000

20 years fixed

1.25% effective interest rate

Rate €1065

5% special repayment possible

Remaining debt after 20 years = €80,000

Including interest, then €255,000 would have been paid after 20 years for €210,000 (290,000€-80,000€)

= €45,000 interest

We have now calculated how the financing of the remaining debt could look like, hope the calculations are correct

at 5% interest in 20 years a refinancing over 10 years would cost a total of €101,000, so a further €21,000 interest until the loan is paid off.

Total costs after the end of financing

1.25% refinancing = €340,000

3.75% refinancing = €351,000

5.00% refinancing = €357,000

etc.

Means, the interest rates would have to rise up to 4.5-5% in the 20 years for the total costs to be identical. Anything higher would make the annuity version more expensive.

I cannot directly see the "catch" of the building savings contract variant(s), but basically many are against building savings contracts.

Am I overlooking something or several factors?

Too many trees, you can’t see the forest anymore :)

If interest rates remain at 1.25% after 20 years, I would be cheaper compared to annuity loan + refinancing, if interest rates rise to 5% I am still identical to annuity loan + refinancing.

With building savings contract you could make higher special repayments, fully repay, etc. With annuity loan I am always bound for time x.

I am neither a fan nor opponent of building savings contracts, but annuity loans are preferred everywhere.

Have we made calculation errors in the whole matter or...

We are more than thankful for tips or advice, because soon we have to decide how to finance?

Greetings from Saarland