For me, the following relationship between the key interest rate and mortgage financing arises:

Ok. Even if it no longer has anything to do with the original topic.

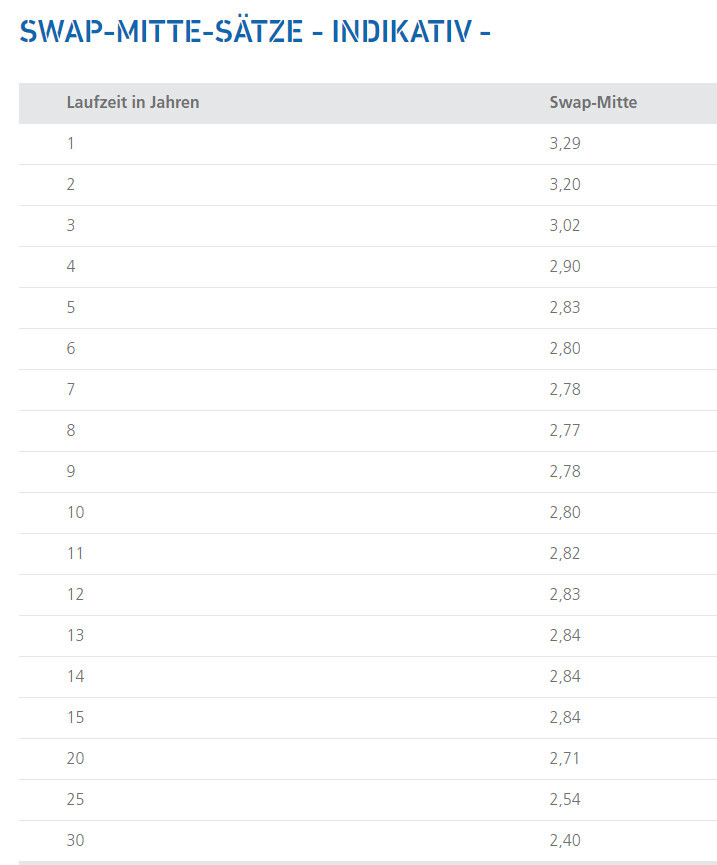

We will break down the whole system of key interest rate and mortgage interest rate for you:

What is the key interest rate?

The key interest rate refers to the interest rate at which credit institutions can borrow money from the central banks. The key interest rate therefore reflects the price that credit institutions have to pay for new funds. For Germany and the other countries of the euro area, the European Central Bank (ECB) sets the key interest rate – more precisely, the ECB Governing Council, which forms the highest decision-making body of the ECB.

The ECB is responsible, among other things, for price stability in the euro area. Because stable prices enable healthy economic growth and corresponding consumption. Therefore, the ECB tries to control the money supply in the economic cycle, among other things, by adjusting the key interest rate and purchasing government and corporate bonds.

There are a total of three key interest rates in the euro area. The most important of them is the main refinancing rate.

[*]The main refinancing rate: In general usage, this is also called the ECB key interest rate or simply the key interest rate. It determines the interest rate at which credit institutions can borrow money from the ECB on a short-term basis.

[*]The deposit rate: This is the interest rate at which commercial banks can park excess money with the ECB overnight.

[*]The marginal lending rate: It indicates the rate at which commercial banks can borrow money from the ECB on a short-term basis.

Overall, the ECB’s key interest rates are an important monetary policy instrument to keep the economy in the euro area balanced and to enable a stable price level. When the economy is doing well, the ECB withdraws money from the economic cycle. If the economy is to be stimulated, it supplies money. Thus, the currently low key interest rate is intended to stimulate inflation and the economy in the euro area.

Is there a direct connection between the ECB key interest rate and mortgage interest rates?

The ECB key interest rate only influences current mortgage interest rates indirectly. A reaction chain can occur but does not have to.

Usually, the ECB announces a change in the key interest rate long in advance, even before it changes the key interest rate. Both the money market for short-term investments and the capital market for long-term investments react already upon an announcement of a key interest rate change. If the key interest rate actually changes, the money market usually reacts even more strongly because short-term interest rate changes can be passed on to customers faster.

Long-term investments, on the other hand, are less flexible. They set their course already upon the announcement of a key interest rate change. If there is an ECB key interest rate change, no further adjustment is necessary.

A mortgage financing counts as a long-term investment. Here, announcements about interest rate changes often have a time-delayed and dampened effect compared to movements on the money market.

Covered bonds for the refinancing of banks

Banks usually borrow the money for a mortgage financing, i.e., the loan amount, from an investor. Experts then speak of refinancing. For the refinancing of mortgage loans, banks mainly use the trading of securities.

If an investor lends the bank the money for a mortgage financing – often institutional investors such as fund companies or insurance companies – they receive a fixed interest rate over the duration of the term in return. In technical jargon, this is called a "covered bond." They are considered secure bonds because they are associated with collateral, mostly a property. Furthermore, covered bonds are regulated by law through the Covered Bonds Act ([Pfandbriefgesetz] (PfandBG)).

The refinancing process of mortgage financing can roughly be divided into the following steps:

[*]The customer approaches the bank and wants to conclude a mortgage financing.

[*]The bank borrows the money for the mortgage financing from investors on the capital market. For this purpose, it issues covered bonds to the investors. The collateral consists either of properties owned by the bank itself or the rights to the properties of its mortgage clients.

[*]In return for their investment, the investors receive interest and the right to realize the property in case of payment defaults.

[*]The bank passes the money on to the customer as the loan amount for their mortgage financing.

The interest rate that the bank has to pay the investor for the borrowed money, called the covered bond interest rate, is passed on to the customer with a small margin. The customer pays back the loan with interest to the bank over many years.

Thus, the bank fulfills its obligations to the investor and simultaneously achieves an economic profit. Mortgage interest rates therefore depend directly on the level of the covered bond interest rate. The key interest rate, on the other hand, has no direct influence on mortgage interest rates.