Carefully checking the total costs seems very low to me, unless it’s being built somewhere in the middle of nowhere with a lot of own labor. I would choose option 1, nice and uncomplicated, long-term security. The building blocks with different terms can cause problems when refinancing.

The total costs are fine so far. Offers are available.

Unfortunately, I can’t follow that at all. You just have to take the trouble once to calculate the accrued interest and compare it:

Option 2 consists of three components. The total annuity amounts to €1,689.59 per month for the first 10 years (€1,169.05 + €220.54 repayment phase + €300.00) – whereas for option 1: €1,749.30.

The uncertainty with option 2 comes after 10 years, as then the interest lock on the KfW 124 loan expires. I would save €302.87 monthly on a fixed deposit account alongside the total annuity; resulting in a total monthly burden of €1,992.45. After 10 years, at 2.5% interest (which is currently achievable), you will have saved €41,328 to repay the KfW124 loan. If interest is only 1.5%, you have around €2,000 less – the risk is manageable.

To avoid comparing apples and oranges, you could put aside €250 monthly in option 1 (total monthly burden €1,999.30), to make special repayments of €3,040 annually (including 2.5% savings interest).

What is the result now?

Option 1 (assuming a constant interest rate for 20 years) you are debt-free after 24 years and 8 months and have paid €189,484.54 in interest.

Option 2 (assuming a constant interest rate for the annuity loan after 15 years) you are debt-free after 25 years and have paid €147,448.35 in interest, i.e. €43,258 less – the interest rate risk for the 5 years shorter interest lock period of the annuity loan can’t be that big – because you also have that risk with option 1 after 20 years.

Excel is your friend!

Thanks for the calculations.

Correct me if I’m wrong, but with a fixed deposit account you can’t set up a savings plan and have to fix a single amount.

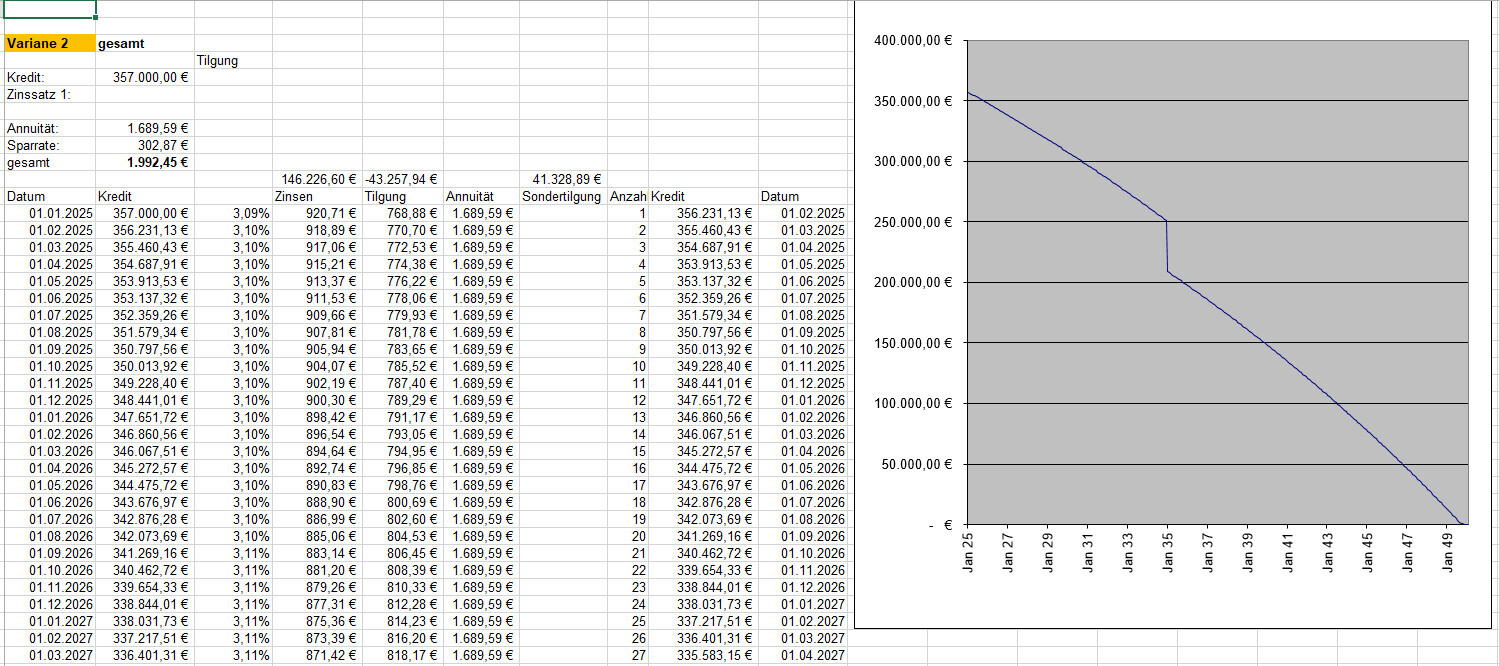

and here is option 2... word for word exclamation mark

Why does the interest rate change over the course of the term?

Have you already looked into the family housing subsidy from SAB? The funding amount is somewhat lower, but you do not need the KfW loan for that.

We have. However, the income limits there are much lower and there are limits on living space and total costs that strongly restrict. For 3 persons (2 adults + 1 child) you are only allowed to build 130 m². This house may then not cost more than €480,000.

----

Setting aside a savings amount would be possible in principle, but you often read that people don’t do special repayments anyway.

I would like to go back to a question from my initial post:

[*]Set the annuity loan to a 10-year fixed interest period and then combine the remaining debt and refinance afterward.

-> Here you get about 0.2% interest advantage compared to 15 years. However, I see difficulties that the terms of AD and KfW end simultaneously (keyword repayment-free starter years). What are your experiences in this regard?