Planning/Financing

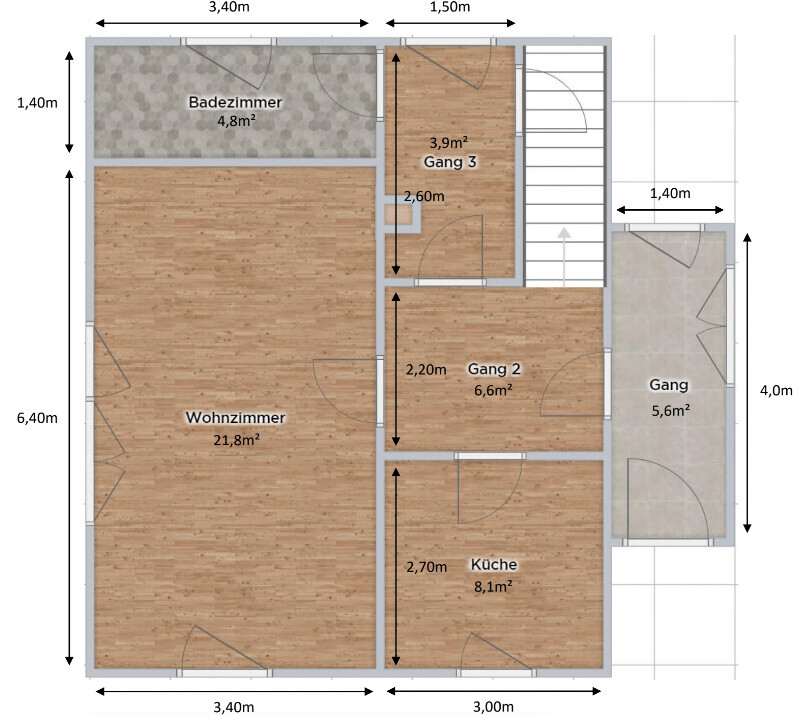

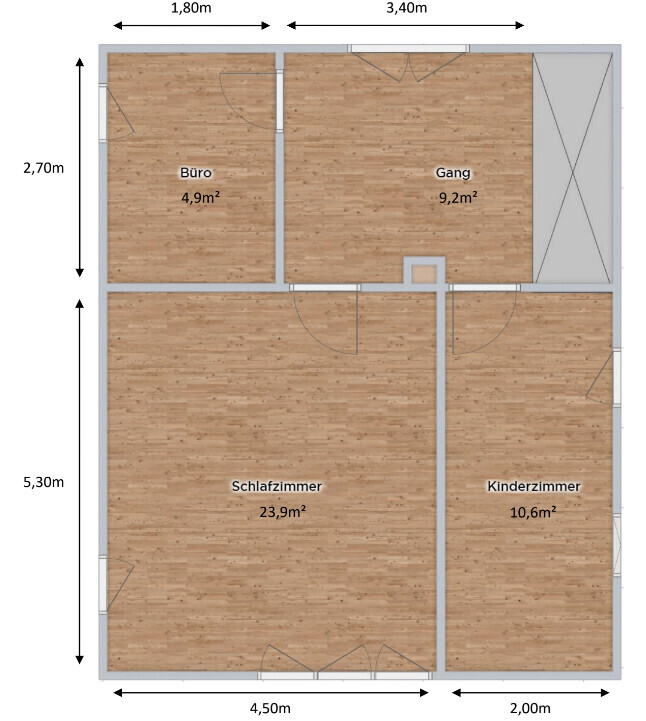

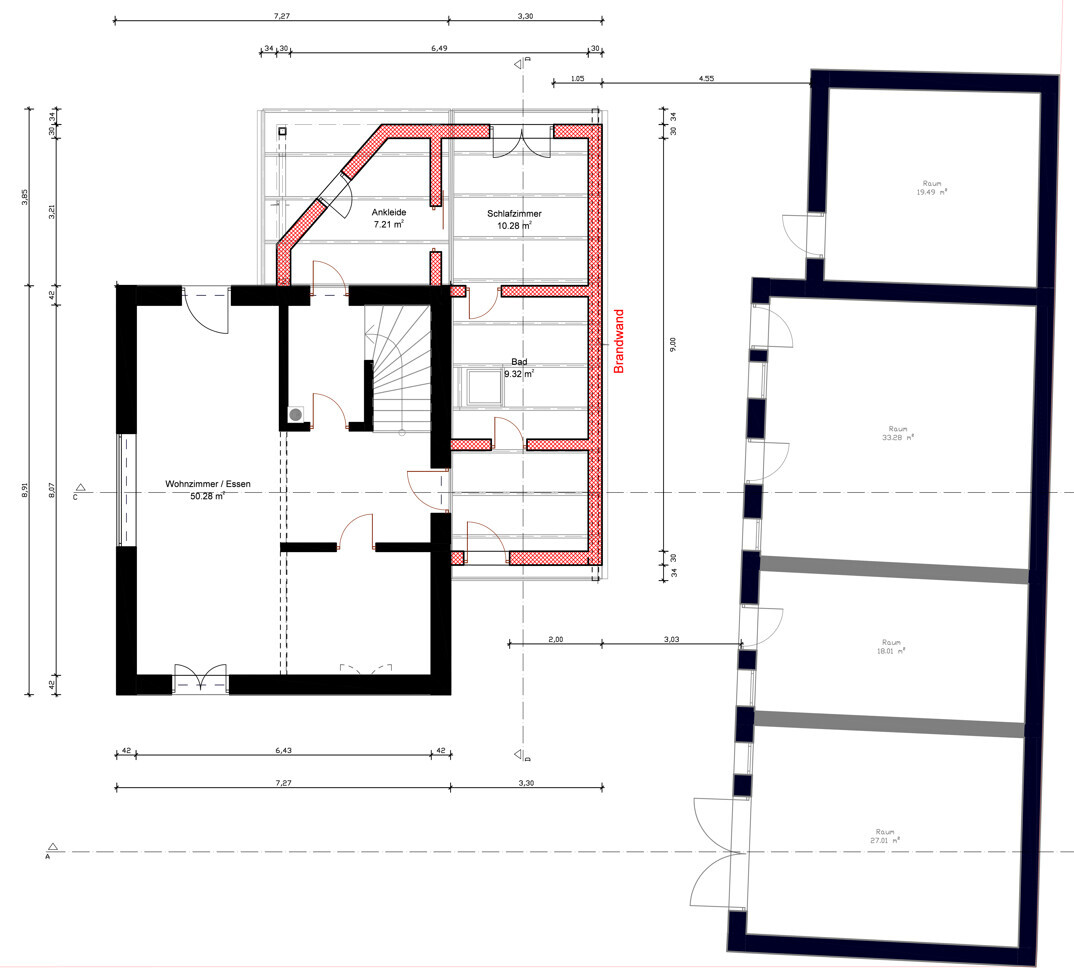

We have arrived at September 2020 and the planning has meanwhile taken shape. Based on the existing floor plans, the rooms should be divided as follows. The existing floor plans were not yet completely to scale at this point in time, but they suffice for illustration. :)

The ground floor

The upper floor

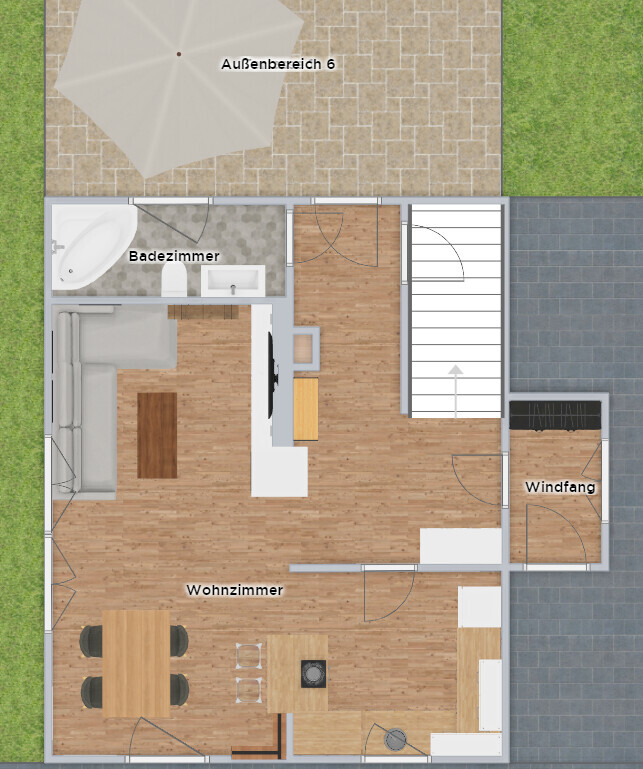

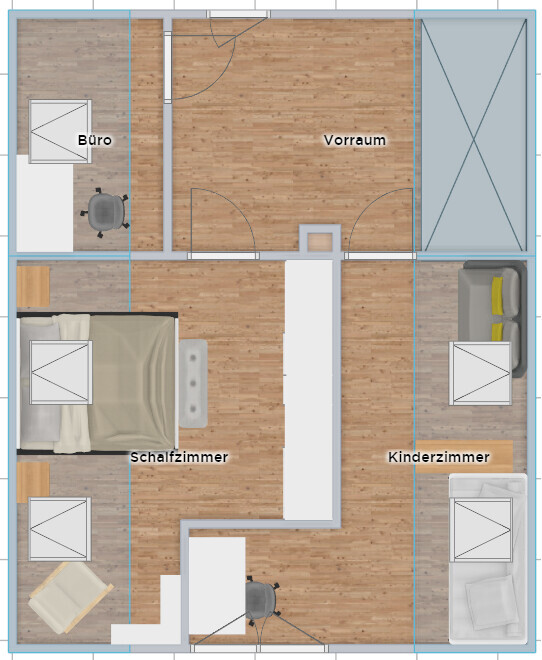

At the same time, I created an initial plan for the extension, which was discussed as a draft with the building authority. Thanks to short channels of communication, I was given a preliminary oral approval for an extension within a few days, with special consideration of fire protection. This ultimately led to the decision to relocate the existing bathroom from the old house into the extension and to build a children’s/guest bathroom on the upper floor. Accordingly, the living room has become significantly larger and offers direct access to the terrace. The extension is planned for three years from now, and the existing house will be insulated at the same time.

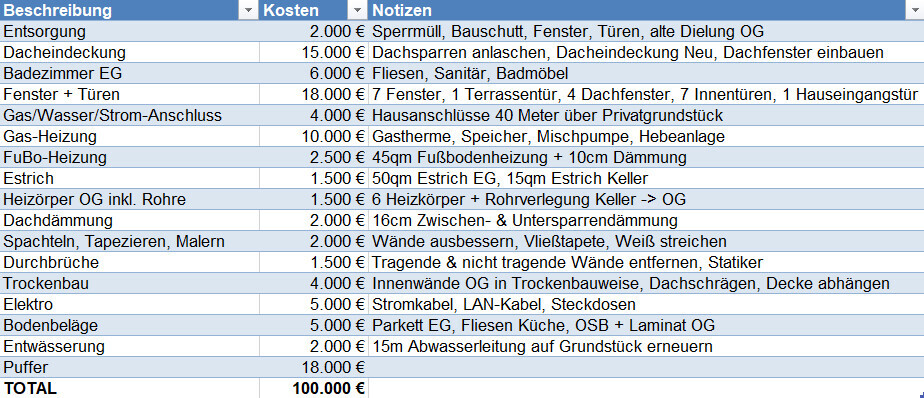

Now to the details of cost planning and financing. Of course, the planned extension is not included here. Sources of information included offers, websites, and consultations with acquaintances and relatives. Since we have electricians, plumbers, carpenters, and structural engineers within our family and circle of friends, some costs can be balanced out with bratwurst and beer. ;)

The next step was to visit Dr. Klein to discuss financing options. At this point, I can only highly recommend hiring a credit broker. We were absolutely positively surprised by the expertise and experience with which we were helped here. Especially on the topic of renovation and KfW loans, we received many suggestions, which is why we ultimately decided to forego KfW.

In the end, we settled with Sparkasse Leipzig, which offered us the best overall package.

Due to the upcoming baby, parental leave for both of us, and job changes, it was important to us that the installment stays below €1,200 and that we have the possibility to make special repayments.

The key figures of the financing:

Household net income: |

€5,550 |

Without bonuses and special payments |

Household net income including parental leave |

€3,800 |

|

|

|

|

Necessary expenses |

-€1,170 |

Car, insurance, groceries, daycare |

Optional expenses |

-€600 |

Entertainment, dining out, vacation |

Savings plan for retirement |

-€800 |

ETF, stocks |

|

|

|

Remaining |

€2,980 |

|

|

|

|

Total loan |

€315,000 |

|

Of which renovation loan |

€100,000 |

|

|

|

|

Interest rate (15 years fixed) |

1.29% |

|

Monthly installment |

€1,126 |

|

Remaining debt after 15 years |

€168,000 |

|

Possible special repayment per year |

€15,000 |

|

If you factor in that we can make special repayments of €6,000 annually (bonus payment, 13th salary), after 15 years there will still be a remaining debt of €75,000. We can live with that with a clear conscience and have the house paid off by age 45, should interest rates rise further and we pay the remaining debt out of equity.

Additionally, there is enough leeway to save money for the extension and take out a second financing.

The reason we ultimately chose Sparkasse was that we do not have to provide proof of use for the renovation loan and at the same time it is my house bank.

1.5 months have passed since the first viewing and we have received the bank’s approval. Next, we went to the notary to register the right of way in the land register. The house is accessed by a 20-meter private road, which is used by three parties.

In November 2020, we finally signed the purchase contract.