Hey ho, I'm bringing the old thread back to life.... We have pushed the house-building topic further and have now also (much faster than expected) received the building permit!

Not much has changed in the initially described situation, except that the second junior is now going to daycare, of course everything has become more expensive "along the way," and we have corrected the flat rates previously used in our calculation (kitchen, painter, flooring) to more realistic and offer-based values (i.e. significantly upwards). In addition, we have planned a photovoltaic system with storage (20-25 k€) as another cost driver and had a nice design created by a landscape architect (whose complete implementation would easily cost 50-70 k€, but can also be implemented modularly over the next XX years, the main thing is that the basic work is done first).

Those were the "expensive" developments – but there is also more positive financial news: I am now on the way to becoming a civil servant (meaning a bit more cash in the pocket and soon no longer paying the maximum rate in the statutory health insurance, but the cheap supplementary tariff in private health insurance), my wife will start part-time again next week, we have further increased our equity, are now more confident regarding the manageable burden (which was not the case from the beginning if you read the thread completely ;)) and will take out a private loan with initially at least 5 years without repayment from my parents. The KfW repayment subsidy will also be fine, but we have consciously not priced that money in yet.

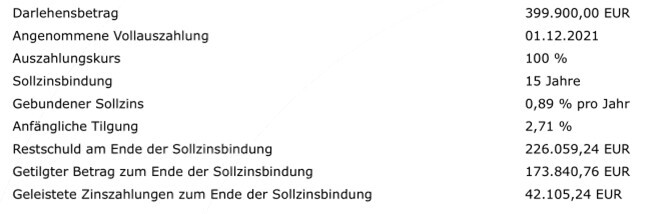

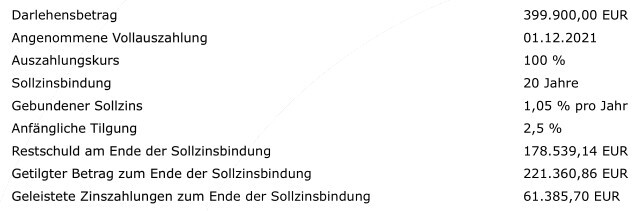

We are still aiming for a loan of €400,000 with a monthly rate of roughly €1,200 and have always planned the option of special repayments. We have collected many different financing offers and are now undecided.... a) ....prefer to take a better interest rate for 15 years or b) fix the current low interest rate level for 20 years (or even longer)?

a) – here the question is: What interest rate do you get after the effective 0.91% on the remaining ~€226k as a follow-up? It can hardly get better.

b) – here we pay already about €12k more interest at an effective 1.07% over the comparable period of 15 years, which roughly corresponds to an average year of repayment performance.

For 25 years or more, the interest then rises somewhat more comparatively to ~1.25%. As a full repayment loan (around 32 years) we end up at ~1.3%.

We are more security-oriented, so we tend toward the longer fixed interest rate – on the other hand, it pains me more to see the interest written in black and white. What to do?

And in general: 0.91% effective is okay, right?

Thanks in advance and best regards from the Rhineland!