NanDe

2017-09-11 12:04:01

- #1

Hello,

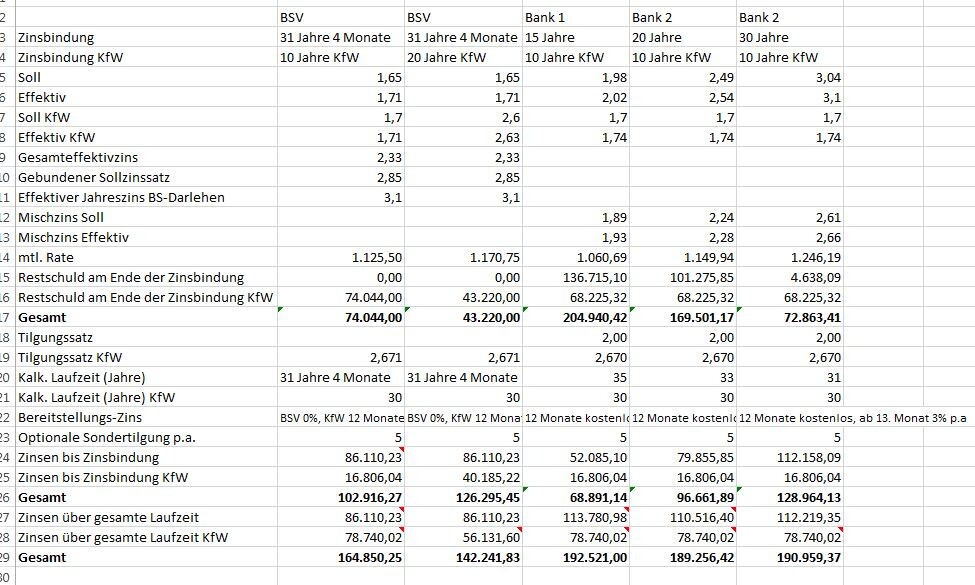

I have often read here that a building savings loan is not recommended. We have been offered a building savings contract and classic annuity loans. To compare them, I have created the following overview. Have I forgotten to consider anything in the comparison? For the KfW loan, a fixed interest rate of 7% was used, and for the other loans, 5%.

Thank you for your help

Nancy

I have often read here that a building savings loan is not recommended. We have been offered a building savings contract and classic annuity loans. To compare them, I have created the following overview. Have I forgotten to consider anything in the comparison? For the KfW loan, a fixed interest rate of 7% was used, and for the other loans, 5%.

Thank you for your help

Nancy