pffreestyler

2018-08-07 19:30:45

- #1

Hello,

a total of €200,000.00 is to be financed.

I currently have two offers available.

1. Interest-only loan with repayment through a home savings contract

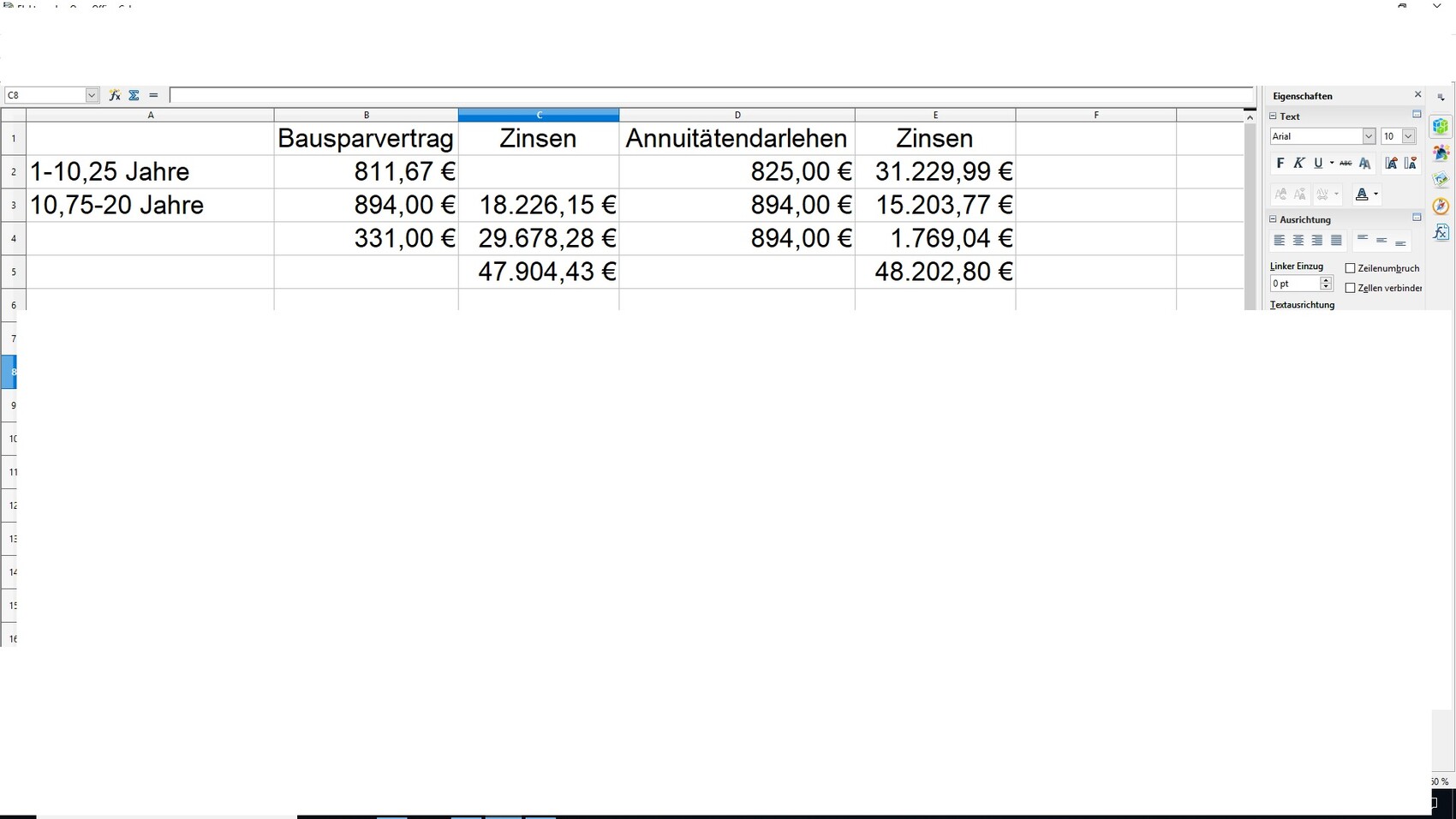

€110,000.00 over a total of 20 years 6 months:

10 years 2 months: nominal interest rate 0.88 %, installment €480.67

10 years 4 months: nominal interest rate 2.15 %, installment €563.00

Effective annual interest rate for the entire term from the disbursement of the interest-only loan 1.49 %

Effective annual interest rate from allocation 2.44 %

Interest costs: €18,226.15

€90,000.00 over 27 years 9 months:

14 years 8 months: nominal interest rate 1.49 %, installment €331.00

14 years 8 months: nominal interest rate 2.85 %, installment €331.00

Effective annual interest rate for the entire term from the disbursement of the interest-only loan 2.85 %

Effective annual interest rate from allocation 3.10 %

Interest costs: €29,678.28

Total interest: €47,904.43

In this variant, my Wohnriesterguthaben of €4,600.00 is included. That saves me about €3,000.00 in interest and the small loan is repaid about 3 years earlier. Wohnförderkonto is a familiar term to me. I would have allowances of €5,071.10 and additional tax benefits of €14,333.00. Upon retirement, about €16,500.00 would be due. So it is not a disadvantage.

Total installments:

10 years: €811.00

10 years: €894.00

7 years: €331.00

2. Variant via finance broker -> lender insurance

€150,000.00 with 20 years fixed interest at 1.86 % - installment €550.00

Interest costs after 20 years: €39,778.35 - outstanding debt €57,778.35. Here I assumed 5 % interest and an installment of €775.00, since then the second component is paid off. Interest costs €11,555.58. Makes a total of €51,333.93

€50,000.00 KFW 124 10 years fixed interest at 1.65 % installment €210.00

Interest costs €7,068.14 - outstanding debt €33,523.21

Incidentally, I am already saving into existing home savings contracts with a total of almost €100.00, with which after 10 years I will repay the outstanding debt of the KfW loan and additionally still have almost €3,000.00 privately in cash available. This then costs me almost €900.00 interest over 8 years with an installment of €225.00.

Thus, I am at total interest of €59,307.02 for both components.

Total installments:

10 years: €860.00

8 years: €775.00

6 years: €775.00

Thus, variant 1 is clearly the winner at first glance with similarly long terms. However, it must be taken into account that the monthly burden partly diverges. Since I can make unlimited special repayments and changes to the repayment rate in variant 1 and can repay 5 % special repayments annually and change the repayment rate 3 times free of charge in variant 2, I calculated variant 2 in Excel using the installments from variant 1 with a repayment calculator:

The interest costs are now practically the same. On the one hand, I know that home savings loans are always advised against here, but do I see it so that this is still the better option? Disadvantage: Wohnförderkonto for my head - financially no disadvantage

Advantage: after 20 years, €550.00 less in installment payments are due. If I consistently put the free capital into special repayments, the interest will certainly be reduced by a noticeable amount again. Another advantage is that I do not have to include the existing home savings contracts. Of course, I would reduce the savings significantly, but I have them in reserve for renovation emergencies. Moreover, my Wohn-Riester is used, which I could not use with an annuity loan. I would probably cancel it at a loss or leave it.

How do you evaluate the offers? I have other annuity loans from other banks, but they are worse than the ones mentioned above.

a total of €200,000.00 is to be financed.

I currently have two offers available.

1. Interest-only loan with repayment through a home savings contract

€110,000.00 over a total of 20 years 6 months:

10 years 2 months: nominal interest rate 0.88 %, installment €480.67

10 years 4 months: nominal interest rate 2.15 %, installment €563.00

Effective annual interest rate for the entire term from the disbursement of the interest-only loan 1.49 %

Effective annual interest rate from allocation 2.44 %

Interest costs: €18,226.15

€90,000.00 over 27 years 9 months:

14 years 8 months: nominal interest rate 1.49 %, installment €331.00

14 years 8 months: nominal interest rate 2.85 %, installment €331.00

Effective annual interest rate for the entire term from the disbursement of the interest-only loan 2.85 %

Effective annual interest rate from allocation 3.10 %

Interest costs: €29,678.28

Total interest: €47,904.43

In this variant, my Wohnriesterguthaben of €4,600.00 is included. That saves me about €3,000.00 in interest and the small loan is repaid about 3 years earlier. Wohnförderkonto is a familiar term to me. I would have allowances of €5,071.10 and additional tax benefits of €14,333.00. Upon retirement, about €16,500.00 would be due. So it is not a disadvantage.

Total installments:

10 years: €811.00

10 years: €894.00

7 years: €331.00

2. Variant via finance broker -> lender insurance

€150,000.00 with 20 years fixed interest at 1.86 % - installment €550.00

Interest costs after 20 years: €39,778.35 - outstanding debt €57,778.35. Here I assumed 5 % interest and an installment of €775.00, since then the second component is paid off. Interest costs €11,555.58. Makes a total of €51,333.93

€50,000.00 KFW 124 10 years fixed interest at 1.65 % installment €210.00

Interest costs €7,068.14 - outstanding debt €33,523.21

Incidentally, I am already saving into existing home savings contracts with a total of almost €100.00, with which after 10 years I will repay the outstanding debt of the KfW loan and additionally still have almost €3,000.00 privately in cash available. This then costs me almost €900.00 interest over 8 years with an installment of €225.00.

Thus, I am at total interest of €59,307.02 for both components.

Total installments:

10 years: €860.00

8 years: €775.00

6 years: €775.00

Thus, variant 1 is clearly the winner at first glance with similarly long terms. However, it must be taken into account that the monthly burden partly diverges. Since I can make unlimited special repayments and changes to the repayment rate in variant 1 and can repay 5 % special repayments annually and change the repayment rate 3 times free of charge in variant 2, I calculated variant 2 in Excel using the installments from variant 1 with a repayment calculator:

The interest costs are now practically the same. On the one hand, I know that home savings loans are always advised against here, but do I see it so that this is still the better option? Disadvantage: Wohnförderkonto for my head - financially no disadvantage

Advantage: after 20 years, €550.00 less in installment payments are due. If I consistently put the free capital into special repayments, the interest will certainly be reduced by a noticeable amount again. Another advantage is that I do not have to include the existing home savings contracts. Of course, I would reduce the savings significantly, but I have them in reserve for renovation emergencies. Moreover, my Wohn-Riester is used, which I could not use with an annuity loan. I would probably cancel it at a loss or leave it.

How do you evaluate the offers? I have other annuity loans from other banks, but they are worse than the ones mentioned above.