Gregor_K

2022-09-27 20:20:26

- #1

Hello,

since interest rates have risen sharply in recent months, I am thinking about the best way to finance the construction project. I received information from Interhyp that another interest rate increase to 0.51% is planned for next Friday. That would put us at about 4% and we would have to stop the construction project, build a "smaller" house, or bring in more equity instead of just financing the ancillary construction costs.

About us...

- married

- 2 adults with 3 children

- household income €7,500, including child benefits and a variable portion of about €1,100 (the variable portion is paid out annually, always for 14 years)

- the house to be financed is €650,000 and depending on the interest rate we will bring in up to €50,000 additional equity

- plot with equity is already available

- ancillary construction costs will be paid with equity

- at least €160,000 equity plus the value of the plot are available in total (we do not want to use all of it)

This week I have looked into alternative financing methods and in particular came across the flex loan. With the flex loan, the interest rate is reset every 3 months, linked to the EURIBOR. Special repayments are also possible every 3 months. Interhyp sent me an offer today for a flex loan and it is very tempting. So the question is, where is the catch? Is creditworthiness checked every 3 months or only once? What I don't want is to be told at some point that my income is no longer sufficient and that the loan has to be repaid. I can live with fluctuations in the rate because I can compensate for them with sufficient equity. Of course, I still don't feel completely comfortable with the thought.

Offer from Interhyp:

Loan amount: 650,000

Nominal interest rate: 0.57%

Effective annual interest rate: 0.61%

Rate: €1,392.08

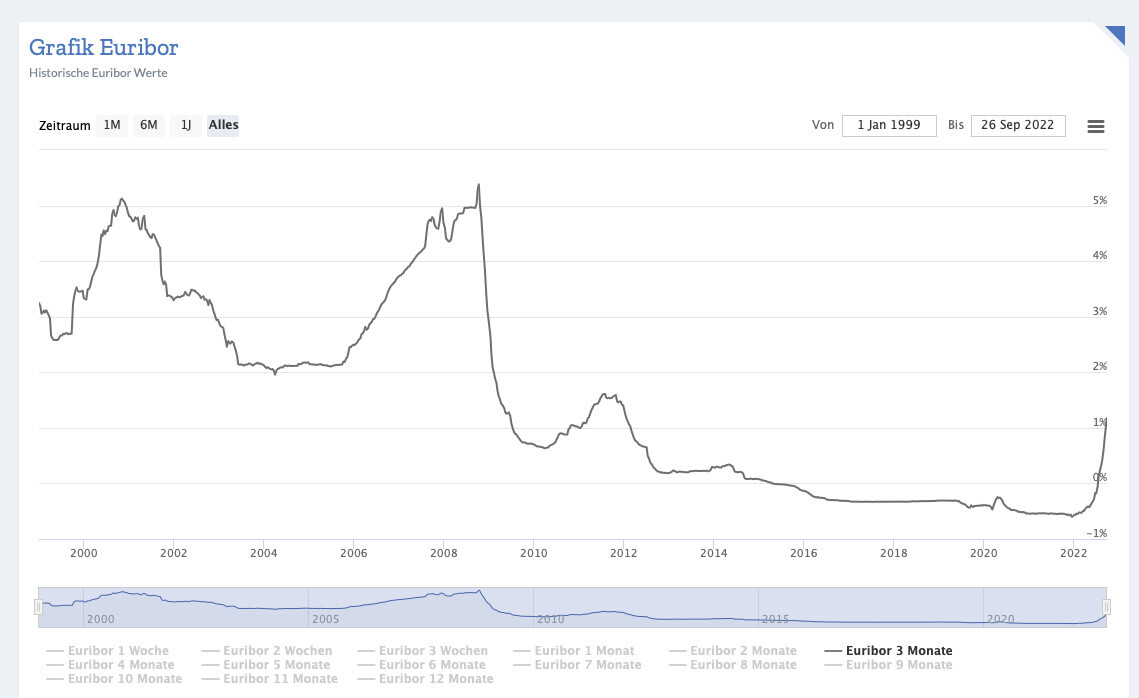

I have attached the long-term EURIBOR chart for you, which clearly shows that it has not been above 6% in the last 20 years. We can manage a rate of €2,800, with assumed interest rates of 6% we would be at a rate of about €4,300. That would be additional annual costs of €18,000 which could be offset by equity.

since interest rates have risen sharply in recent months, I am thinking about the best way to finance the construction project. I received information from Interhyp that another interest rate increase to 0.51% is planned for next Friday. That would put us at about 4% and we would have to stop the construction project, build a "smaller" house, or bring in more equity instead of just financing the ancillary construction costs.

About us...

- married

- 2 adults with 3 children

- household income €7,500, including child benefits and a variable portion of about €1,100 (the variable portion is paid out annually, always for 14 years)

- the house to be financed is €650,000 and depending on the interest rate we will bring in up to €50,000 additional equity

- plot with equity is already available

- ancillary construction costs will be paid with equity

- at least €160,000 equity plus the value of the plot are available in total (we do not want to use all of it)

This week I have looked into alternative financing methods and in particular came across the flex loan. With the flex loan, the interest rate is reset every 3 months, linked to the EURIBOR. Special repayments are also possible every 3 months. Interhyp sent me an offer today for a flex loan and it is very tempting. So the question is, where is the catch? Is creditworthiness checked every 3 months or only once? What I don't want is to be told at some point that my income is no longer sufficient and that the loan has to be repaid. I can live with fluctuations in the rate because I can compensate for them with sufficient equity. Of course, I still don't feel completely comfortable with the thought.

Offer from Interhyp:

Loan amount: 650,000

Nominal interest rate: 0.57%

Effective annual interest rate: 0.61%

Rate: €1,392.08

I have attached the long-term EURIBOR chart for you, which clearly shows that it has not been above 6% in the last 20 years. We can manage a rate of €2,800, with assumed interest rates of 6% we would be at a rate of about €4,300. That would be additional annual costs of €18,000 which could be offset by equity.