Stegi

2014-04-06 11:51:50

- #1

We are planning a house in Hannover. The house will cost around 230,000 euros turnkey. Since we have a lot of tree felling to do and the development will not be easy, we are planning with additional construction costs of 70,000 euros. Especially since turnkey in this case also means that painting and flooring still have to be done. We are building as a Kfw55 house! I am 43 years old, my wife 34 years old. Fixed interest period is an issue.

So 300,000 euros will be needed. Unfortunately, only the plot of land can serve as equity. It has a market value of 210,000 euros. 700 sqm at 300 euros each. I am a civil servant at the state level and my wife currently takes care of the upbringing of the children, otherwise employed. Both are borrowers. Our financial situation will continue to develop positively in the coming decades due to inheritance, of course, we do not plan on that and wish all our family members a long, fulfilled life. That's clear!

I have now received 2 offers. I would like to show them to you and maybe some experts here can have a go. Often it is far too non-transparent for me. The first offer is from the Münchener Hypothekenbank. But it expires tomorrow. I therefore feel somewhat pressured. If it is as great as my broker says, then I should actually sign it. A friend told me BER, that such offers always come and the market is hardly moving at the moment. I’ll first show you the offer from Schwäbisch Hall (I do not understand it at all!):

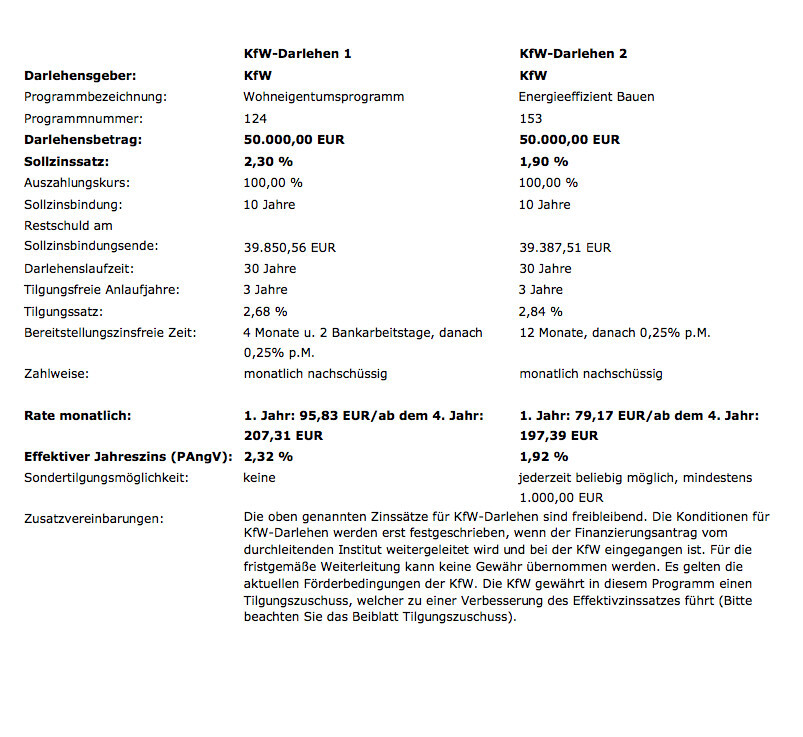

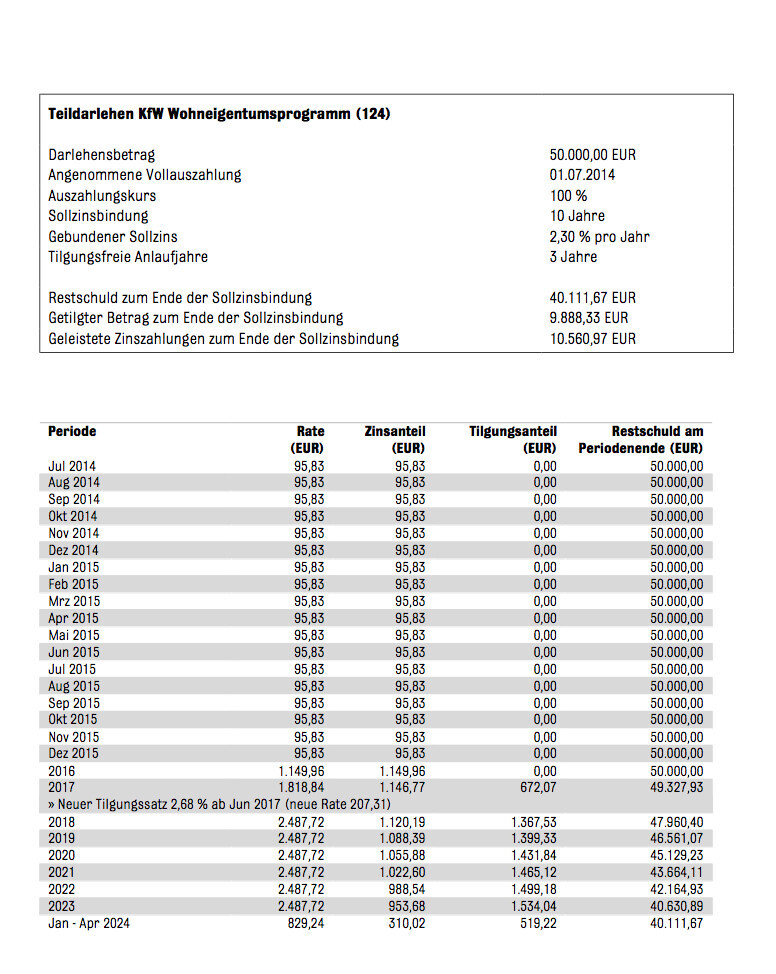

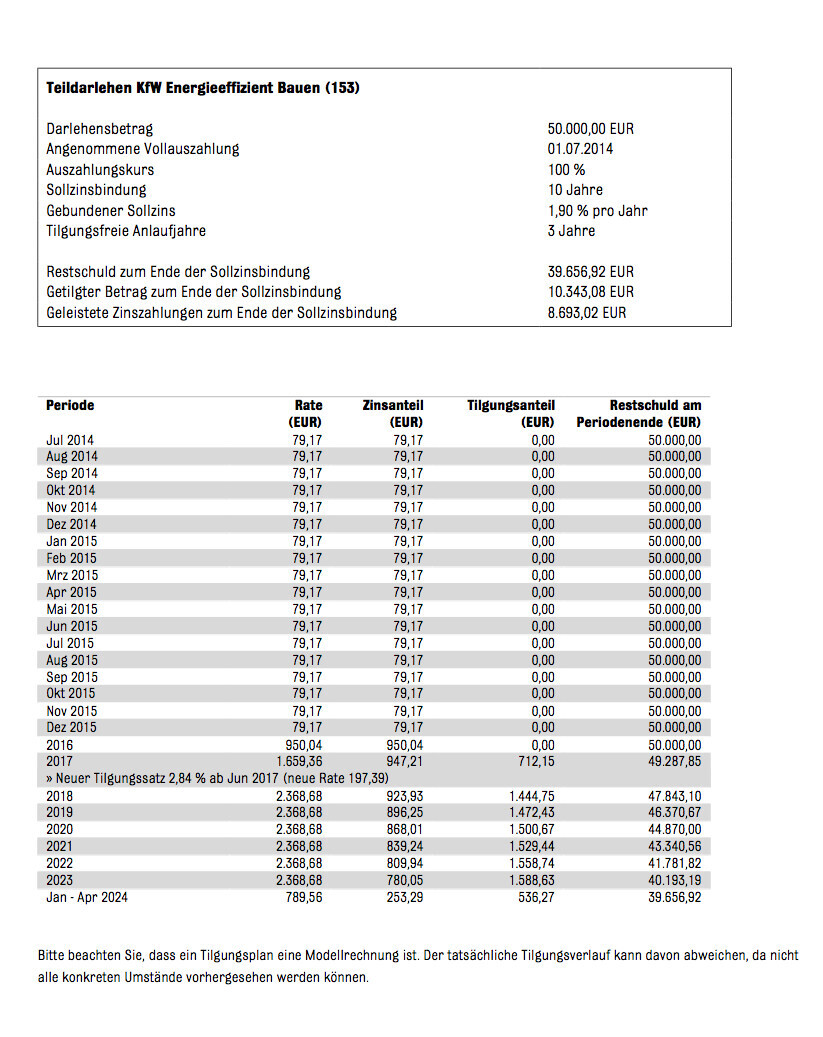

1. KFW loan no. 153 for 50,000 euros Fixed interest period 10 years Interest 1.90% Effective interest 1.92%, repayment-free start years at least 1 year max. 5 years Interest rate 79.17 euros monthly From the 4th year 197.39 euros including 2.84% repayment, remaining loan after 10 years 39,387.51 euros for extension Special repayment at least 1,000 euros anytime Commitment interest from 13th month 3% p.a.

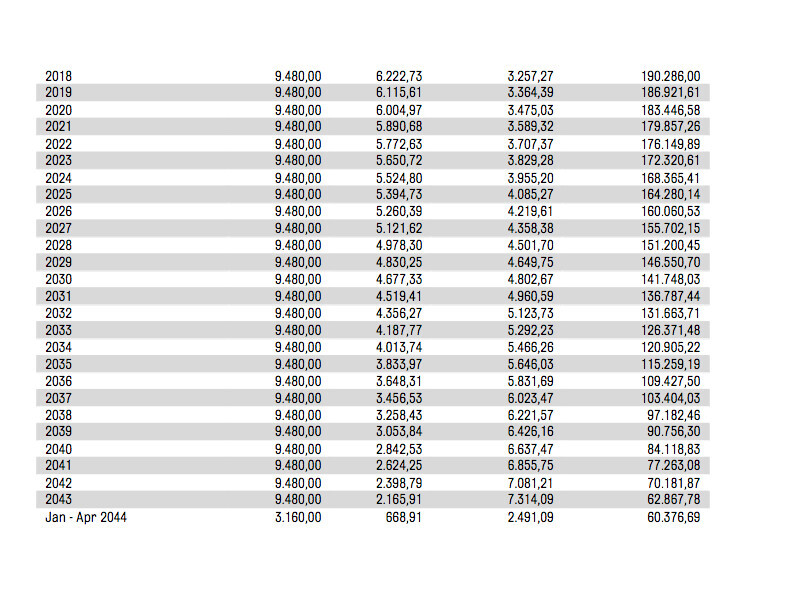

2. Repayment-free loan via the building society Schwäbisch Hall 150,000 euros Fixed interest period 15 years (loan termination possible after 10 years) Interest 3% Effective interest 3.09% Interest rate 375 euros monthly (commitment interest from 13th month 3% p.a.) Interest during construction phase is calculated only on the amount already paid out Only after full disbursement, indirect repayment of 425 euros on the building savings contract takes place Then total monthly burden 800 euros for 15 years Special repayments are possible yearly up to 7,500 euros After 15 years you have a guaranteed interest rate of 2.95%/ effective interest rate 3.14% The interest and repayment payment then amounts to 525 euros monthly, special repayment unlimited possible, If no special repayments occur, your loan will be repaid in 29 years and 5 months.

3. Interest-only loan with redemption by a residential annuity building savings contract 50,000 euros for J. S. Fixed interest period 13 years Interest 2.45% Effective 2.53% After 13 years interest 2.50% / effective 2.77% !! Monthly interest rate 102.08 euros, after full disbursement of the loan plus 70 euros savings rate into a residential annuity building savings contract Special repayment amounting to 2,500 euros p.a. possible in the first 13 years After 13 years Interest 2.50% Effective 2.77% Interest and repayment rate after 13 years monthly 257 euros, unlimited special repayments possible Total duration would be 22 years 5 months The Riester subsidies for the total duration would amount to 14,342 euros!

4. Interest-only loan with redemption by a residential annuity building savings contract 50,000 euros for B. S. Fixed interest period 13 years Interest 2.45% / effective 2.53% After 13 years interest 2.50%/ effective 2.77% !! Monthly interest rate 102.08 euros, after full disbursement of the loan plus 115 euros savings rate into a residential annuity building savings contract Special repayments amounting to 2,500 euros p.a. possible in the first 13 years After 13 years Interest 2.50% Effective 2.77% Interest and repayment rate after 13 years monthly 264 euros, unlimited special repayments possible Total duration would be 24 years and 4 months! The Riester subsidies for the total duration would amount to 3,060.86 euros! Here too, commitment interest from the 13th month of 3% p.a. will be charged. The savings payment into the building savings contracts will only take place after full disbursement. I hope I have provided all details, but the condition is the submission of the complete loan documents as well as presentation of the land registry security.

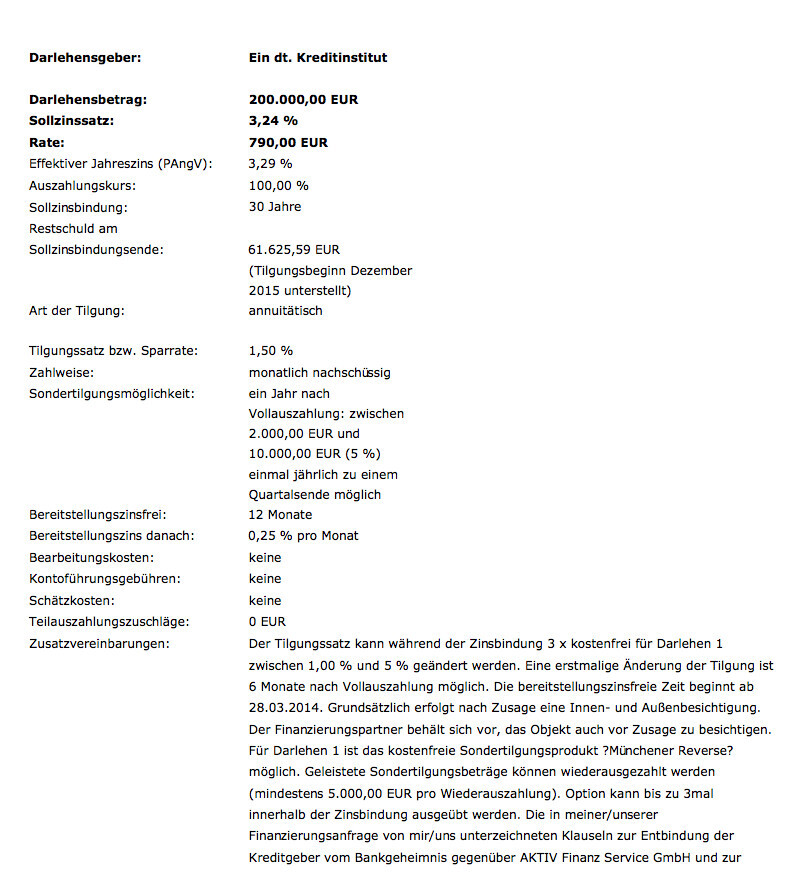

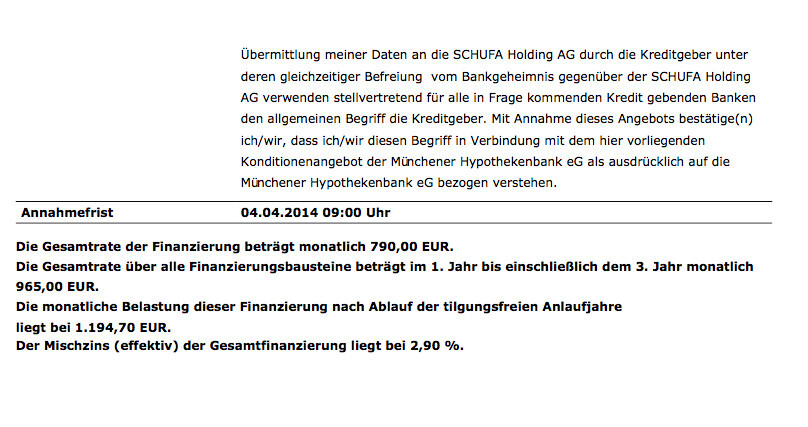

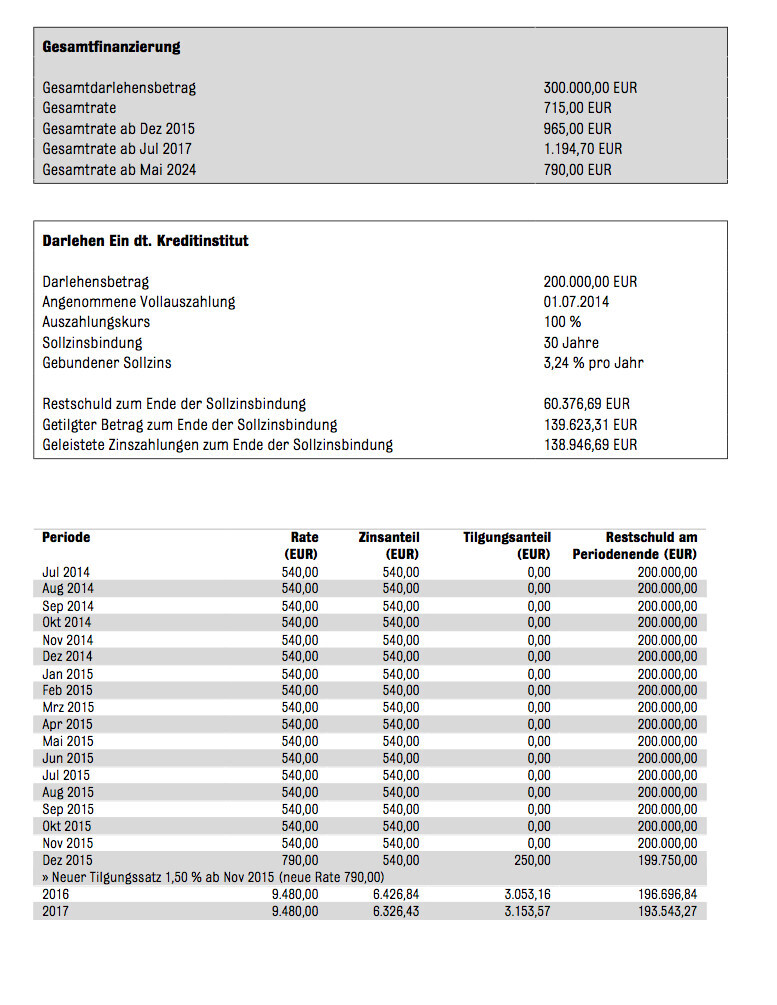

I cannot put the offer from Münchener Hy in here. I have to do it via screenshot. Sorry.

Volksbank Hannover and Stadtsparkasse Hannover have offered me appointments for next week. Also exciting.

I am very curious about your opinions!

I am very curious about your opinions!

Many thanks, says ... Stegi

So 300,000 euros will be needed. Unfortunately, only the plot of land can serve as equity. It has a market value of 210,000 euros. 700 sqm at 300 euros each. I am a civil servant at the state level and my wife currently takes care of the upbringing of the children, otherwise employed. Both are borrowers. Our financial situation will continue to develop positively in the coming decades due to inheritance, of course, we do not plan on that and wish all our family members a long, fulfilled life. That's clear!

I have now received 2 offers. I would like to show them to you and maybe some experts here can have a go. Often it is far too non-transparent for me. The first offer is from the Münchener Hypothekenbank. But it expires tomorrow. I therefore feel somewhat pressured. If it is as great as my broker says, then I should actually sign it. A friend told me BER, that such offers always come and the market is hardly moving at the moment. I’ll first show you the offer from Schwäbisch Hall (I do not understand it at all!):

1. KFW loan no. 153 for 50,000 euros Fixed interest period 10 years Interest 1.90% Effective interest 1.92%, repayment-free start years at least 1 year max. 5 years Interest rate 79.17 euros monthly From the 4th year 197.39 euros including 2.84% repayment, remaining loan after 10 years 39,387.51 euros for extension Special repayment at least 1,000 euros anytime Commitment interest from 13th month 3% p.a.

2. Repayment-free loan via the building society Schwäbisch Hall 150,000 euros Fixed interest period 15 years (loan termination possible after 10 years) Interest 3% Effective interest 3.09% Interest rate 375 euros monthly (commitment interest from 13th month 3% p.a.) Interest during construction phase is calculated only on the amount already paid out Only after full disbursement, indirect repayment of 425 euros on the building savings contract takes place Then total monthly burden 800 euros for 15 years Special repayments are possible yearly up to 7,500 euros After 15 years you have a guaranteed interest rate of 2.95%/ effective interest rate 3.14% The interest and repayment payment then amounts to 525 euros monthly, special repayment unlimited possible, If no special repayments occur, your loan will be repaid in 29 years and 5 months.

3. Interest-only loan with redemption by a residential annuity building savings contract 50,000 euros for J. S. Fixed interest period 13 years Interest 2.45% Effective 2.53% After 13 years interest 2.50% / effective 2.77% !! Monthly interest rate 102.08 euros, after full disbursement of the loan plus 70 euros savings rate into a residential annuity building savings contract Special repayment amounting to 2,500 euros p.a. possible in the first 13 years After 13 years Interest 2.50% Effective 2.77% Interest and repayment rate after 13 years monthly 257 euros, unlimited special repayments possible Total duration would be 22 years 5 months The Riester subsidies for the total duration would amount to 14,342 euros!

4. Interest-only loan with redemption by a residential annuity building savings contract 50,000 euros for B. S. Fixed interest period 13 years Interest 2.45% / effective 2.53% After 13 years interest 2.50%/ effective 2.77% !! Monthly interest rate 102.08 euros, after full disbursement of the loan plus 115 euros savings rate into a residential annuity building savings contract Special repayments amounting to 2,500 euros p.a. possible in the first 13 years After 13 years Interest 2.50% Effective 2.77% Interest and repayment rate after 13 years monthly 264 euros, unlimited special repayments possible Total duration would be 24 years and 4 months! The Riester subsidies for the total duration would amount to 3,060.86 euros! Here too, commitment interest from the 13th month of 3% p.a. will be charged. The savings payment into the building savings contracts will only take place after full disbursement. I hope I have provided all details, but the condition is the submission of the complete loan documents as well as presentation of the land registry security.

I cannot put the offer from Münchener Hy in here. I have to do it via screenshot. Sorry.

Volksbank Hannover and Stadtsparkasse Hannover have offered me appointments for next week. Also exciting.

Many thanks, says ... Stegi