MartinaW

2017-09-14 21:04:27

- #1

Hello everyone,

my question might be a bit off-topic and basically does not directly relate to construction financing. After my mother (a retiree) was diagnosed with severe cancer six months ago, I am trying to get her debts and finances back on track because she is just barely making ends meet.

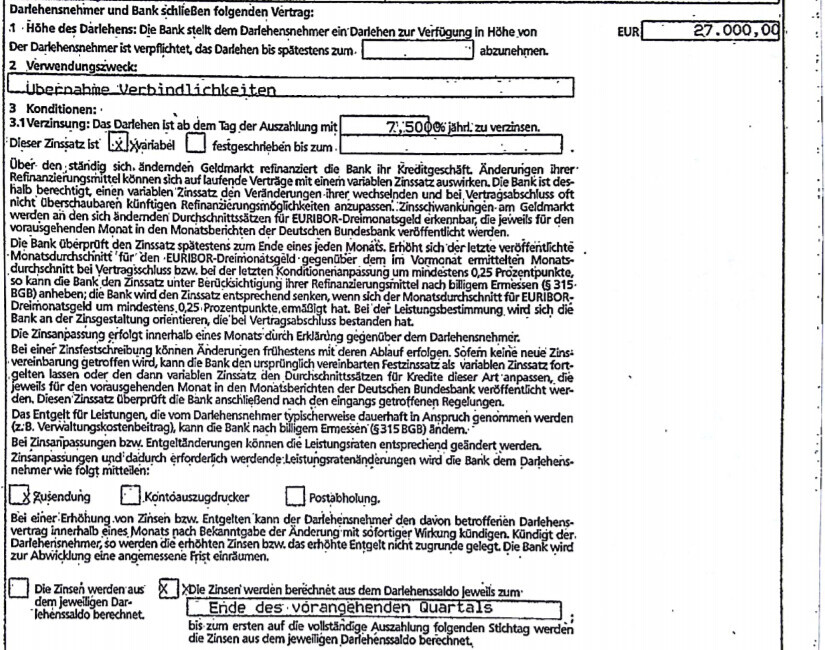

One of the countless issues is a remaining debt she has with the bank. She still has to pay off about 17,000 euros and is paying 190 euros per month (since 2003). Every 3 months, 350 euros are deducted again (interest). I have absolutely no knowledge about this, but someone told me that this is a very high interest rate by today's standards and that she has a loan with a variable interest rate (EURIBOR) (details attached) and the bank actually has to adjust the interest to this (I do not know what this means). In any case, the lady at the bank said that this is not true and that the 350 euros every 3 months is correct and even if the EURIBOR goes down it does not affect my mother’s interest, is that correct? I read in a forum that the interest rates should be adjusted, the bank did not do this and he is now suing. Could you maybe explain to me how this EURIBOR value quantitatively affects the interest she has to pay, because if my mother has to pay more when EURIBOR rises, it really can’t be that she has been paying the same interest since 2003 (how do you actually calculate the current interest you pay per month from what you pay and what interest is charged every 3 months)? I kept pressing the lady at the bank until she suggested refinancing, meaning to dissolve the current loan and grant a new one with a lower interest rate. But I am afraid that I might somehow get my mother into even bigger trouble, although I just want to help her somehow. Do I have to watch out for something, e.g. that a confirmation comes first that the new loan is really granted before she pays off the current one? Then maybe she won’t get a new loan anymore (like at the KSK where they said the risk is too high that she will die soon).

I don’t know what to do and I don’t understand this whole topic at all. Maybe you can help me even if it’s not directly related to building. That would really be nice and it would really help me.

Best regards

Martina.

my question might be a bit off-topic and basically does not directly relate to construction financing. After my mother (a retiree) was diagnosed with severe cancer six months ago, I am trying to get her debts and finances back on track because she is just barely making ends meet.

One of the countless issues is a remaining debt she has with the bank. She still has to pay off about 17,000 euros and is paying 190 euros per month (since 2003). Every 3 months, 350 euros are deducted again (interest). I have absolutely no knowledge about this, but someone told me that this is a very high interest rate by today's standards and that she has a loan with a variable interest rate (EURIBOR) (details attached) and the bank actually has to adjust the interest to this (I do not know what this means). In any case, the lady at the bank said that this is not true and that the 350 euros every 3 months is correct and even if the EURIBOR goes down it does not affect my mother’s interest, is that correct? I read in a forum that the interest rates should be adjusted, the bank did not do this and he is now suing. Could you maybe explain to me how this EURIBOR value quantitatively affects the interest she has to pay, because if my mother has to pay more when EURIBOR rises, it really can’t be that she has been paying the same interest since 2003 (how do you actually calculate the current interest you pay per month from what you pay and what interest is charged every 3 months)? I kept pressing the lady at the bank until she suggested refinancing, meaning to dissolve the current loan and grant a new one with a lower interest rate. But I am afraid that I might somehow get my mother into even bigger trouble, although I just want to help her somehow. Do I have to watch out for something, e.g. that a confirmation comes first that the new loan is really granted before she pays off the current one? Then maybe she won’t get a new loan anymore (like at the KSK where they said the risk is too high that she will die soon).

I don’t know what to do and I don’t understand this whole topic at all. Maybe you can help me even if it’s not directly related to building. That would really be nice and it would really help me.

Best regards

Martina.