Elina

2019-06-28 20:24:21

- #1

Hello everyone,

we recently considered buying an apartment for my mother. We looked at various apartments, but unfortunately, what you got for your money wasn’t that great. At higher prices, the offers were better, but at some point, we also said, then you might as well buy a house.

Example: apartments for about 40-50,000 around 50-70 sqm. Unfortunately mostly on upper floors, no trash bin space, so you’d have to keep the bin in the apartment and carry it up to the 2nd floor every time (mother has mobility issues and is 67)... plus a 1 sqm bathroom or horrendous monthly fees... well, nothing great.

The problem was that we live 600 km away, and the Ing-Diba at least does not finance construction beyond 200 km on its own request, so the limit was 50k, which is our free mortgage. So a capital raise on our house.

Apartments with reasonable layouts that we liked were then rather around 80k and more.

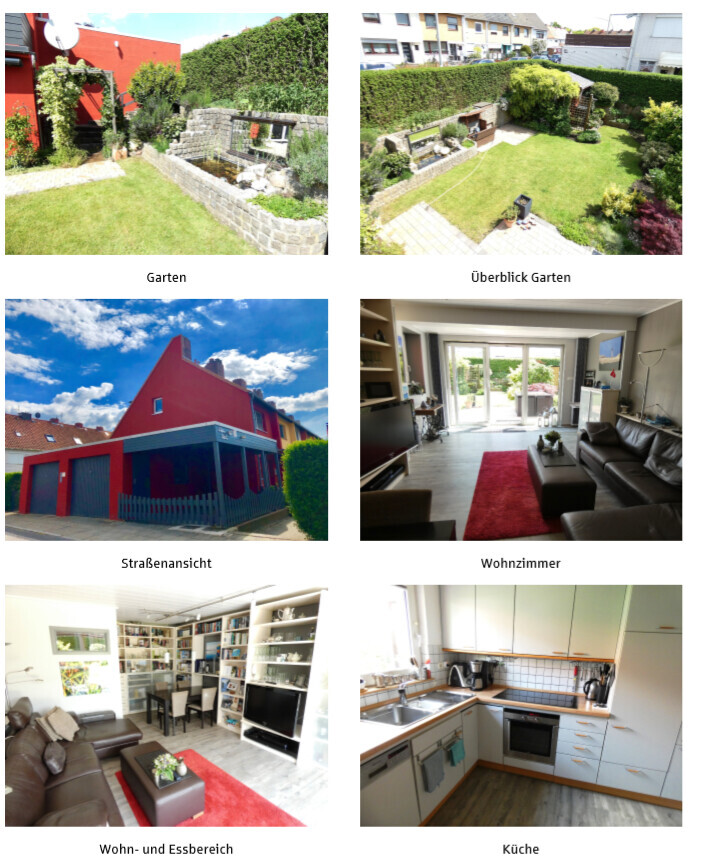

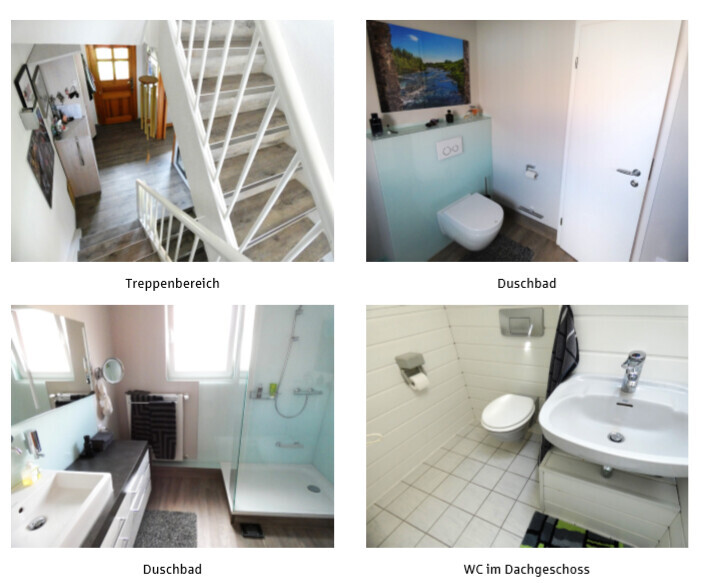

Then we found a house. The perfect one. By chance, my uncle lives next door (he has a car and could drive my mother when she needs to go shopping or to the doctor). The house is in top shape, semi-detached with 90 sqm, 285 sqm plot, so not over the top either. Cost 135,000 plus additional costs (total 152,000). Plus two garages and a carport, all of which can be rented out.

All very well maintained.

And how lucky were we, the house was only listed for 3 days, the viewing was already on the 4th day, there was only one viewing with 14 interested parties, and we got the contract!

Looked at exactly the right moment and snapped it up immediately.

Here is the financing:

120,000 over 10 years with 2% repayment and 1.27% effective interest. Rate 323.00 (mediated through Interhyp to Ing-Diba and lo and behold, the 600 km distance works after all)

50,000 over 5 years with 10% repayment and 0.93% effective interest. Rate 455.42

That leaves about 18,000 for things like a new heating system and other items. The 50,000 is not earmarked, so we have a 90% loan-to-value on the new house despite full financing plus extras.

I deliberately chose the repayment of the smaller loan so high so that it is paid off quickly.

Rental income: 300 from my mother and 150 euros for the three parking spaces. One garage is already rented, my uncle takes the other two. Each net cold rent.

Although I add 330 euros per month, I simply see this as a savings rate. Otherwise, I am really bad at saving; if there is money, it is used immediately, for special repayments or renovations.

So the bank forces me to save, as someone here aptly put it once.

Besides that, we still have the rate for our own house (balance 167,000, rate 770 euros at 3.75% repayment) and a car loan with 3,700 remaining (here I pay 241 regular rate and monthly 500 euros special repayment, so that will be gone soon too).

I know, lower repayment would be better for renting, but I just want to get down from the amount as quickly as possible. When my mother is no longer here, I would of course charge significantly more rent, I think you can ask around 600 euros (plus parking spaces, which are now rented out/are otherwise rented).

What do you think of the financing?

we recently considered buying an apartment for my mother. We looked at various apartments, but unfortunately, what you got for your money wasn’t that great. At higher prices, the offers were better, but at some point, we also said, then you might as well buy a house.

Example: apartments for about 40-50,000 around 50-70 sqm. Unfortunately mostly on upper floors, no trash bin space, so you’d have to keep the bin in the apartment and carry it up to the 2nd floor every time (mother has mobility issues and is 67)... plus a 1 sqm bathroom or horrendous monthly fees... well, nothing great.

The problem was that we live 600 km away, and the Ing-Diba at least does not finance construction beyond 200 km on its own request, so the limit was 50k, which is our free mortgage. So a capital raise on our house.

Apartments with reasonable layouts that we liked were then rather around 80k and more.

Then we found a house. The perfect one. By chance, my uncle lives next door (he has a car and could drive my mother when she needs to go shopping or to the doctor). The house is in top shape, semi-detached with 90 sqm, 285 sqm plot, so not over the top either. Cost 135,000 plus additional costs (total 152,000). Plus two garages and a carport, all of which can be rented out.

All very well maintained.

And how lucky were we, the house was only listed for 3 days, the viewing was already on the 4th day, there was only one viewing with 14 interested parties, and we got the contract!

Looked at exactly the right moment and snapped it up immediately.

Here is the financing:

120,000 over 10 years with 2% repayment and 1.27% effective interest. Rate 323.00 (mediated through Interhyp to Ing-Diba and lo and behold, the 600 km distance works after all)

50,000 over 5 years with 10% repayment and 0.93% effective interest. Rate 455.42

That leaves about 18,000 for things like a new heating system and other items. The 50,000 is not earmarked, so we have a 90% loan-to-value on the new house despite full financing plus extras.

I deliberately chose the repayment of the smaller loan so high so that it is paid off quickly.

Rental income: 300 from my mother and 150 euros for the three parking spaces. One garage is already rented, my uncle takes the other two. Each net cold rent.

Although I add 330 euros per month, I simply see this as a savings rate. Otherwise, I am really bad at saving; if there is money, it is used immediately, for special repayments or renovations.

So the bank forces me to save, as someone here aptly put it once.

Besides that, we still have the rate for our own house (balance 167,000, rate 770 euros at 3.75% repayment) and a car loan with 3,700 remaining (here I pay 241 regular rate and monthly 500 euros special repayment, so that will be gone soon too).

I know, lower repayment would be better for renting, but I just want to get down from the amount as quickly as possible. When my mother is no longer here, I would of course charge significantly more rent, I think you can ask around 600 euros (plus parking spaces, which are now rented out/are otherwise rented).

What do you think of the financing?